When you’re tidying up your documentation for end of tax year, don’t forget to review your debtors. If you are able to write off bad debts, you may be able to claim a tax deduction.

It’s important to do this the right way. It saves time checking later if Inland Revenue asks for more information. And it reduces the likelihood of Inland Revenue rejecting the claim because of insufficient proof.

To do list

- Review your debtors in the lead up to end of tax year.

- Have you taken reasonable steps to recover bad debts?

- Make sure your records show it. If you write off bad debts before 31 March, you may be able to claim a deduction.

- Make sure to give us the details so we can check any GST adjustments are correct.

When has the debt gone bad?

The onus is on you, the taxpayer, to demonstrate that the debt is a bad debt. Inland Revenue’s test is whether a ‘reasonably prudent commercial person concludes that there is no reasonable likelihood that the debt will be paid’. This takes into account:

- time - the length of time a debt has been outstanding is relevant. However, on its own it’s not enough

- effort - demonstrate that you have chased the debt. Notes on the client file documenting follow-up show the effort made trying to collect the debt

- information - note what you hear through business or personal networks. For instance, you might hear the business is in trouble and has defaulted on other creditors

- matters out of your hands - it is out of your control if the debtor has died or disappeared; the business has gone into liquidation or the debt has run beyond a time limit for recovery (e.g. on a mortgage)

Document why you concluded there is no reasonable likelihood that the debt will be paid.

What have you done about it?

Document whatever steps you took to recover the debt, up to and including legal action. Keep it in proportion: if the debt is small, don’t spend more effort chasing it than the debt is worth. If it’s clear that even if you took further action there is still no hope to recover the debt, record what led you to think that.

The kind of debt recovery steps Inland Revenue might expect to find recorded (depending on the size of the debt and circumstances) include:

- reminder notices

- contact by telephone, mail, or email

- a reasonable period of time since the original due date

- a formal demand notice

- legal proceedings for debt recovery with judgment against the debtor and proceedings to enforce

- judgement

- correspondence and notes on steps taken, for example, to claim against the estate or from the

- liquidator or to trace the debtor’s whereabouts

- that you ceased calculating and charging interest and closed the account (although you might

- keep a tracing file open or, in the case of a partial write-off, the account may remain open)

- valuation of any security held against the debt

- sale of any seized or repossessed asset

Writing the debt off

Whatever system your business runs – computer-based accounting software, manual account books, double-entry accounts, or bookkeeping records – there needs to be an entry in your system:

- recording the debt as written off

- by a person with the proper authority to do so

- in the income year or GST taxable period for which you are claiming the deduction

What about GST?

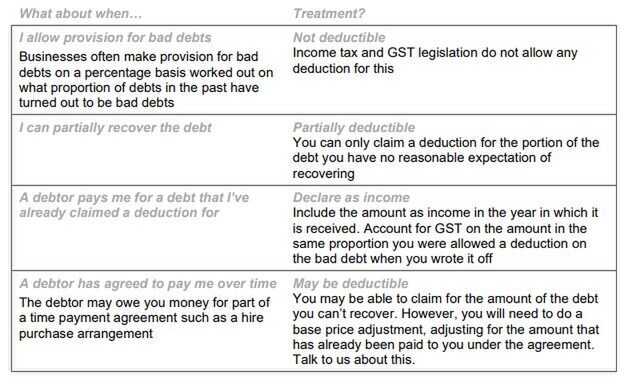

What happens when you made a taxable supply, invoiced for it and returned GST for it, but then your invoice went unpaid and turned out to be a bad debt? You may be able to claim back the GST returned. Or, if it is a partially recoverable bad debt, you may be able to claim back the proportion of GST that relates to the portion of the debt you have no hope of recovering.

Keep in mind

Bad debts are bigger than just claiming a tax deduction. Good debtor management can have a real impact on your cashflow and bottom line. If you would like a better system than you have now, please talk to us.